H.IDX Proprietary Indices

The Hammer Index — Quantitative Benchmarks for the Global Fine Art Market

The Hammer Index® employs a multi-factor scoring model — the Hammer Score (HS) — to evaluate, rank and weight the top 500 artists within each index segment. The complete calibration algorithm is proprietary and held in confidence.

Price Velocity (P). Measures realised auction price performance relative to the segment benchmark, normalised using a hedonic regression framework that controls for lot-level heterogeneity. Rolling 24-month window.

Rarity Index (R). Quantifies supply scarcity using proprietary multi-factor analysis of catalogue coverage, institutional lock-up, and secondary market availability.

Liquidity Depth (V). Composite of transaction velocity, bid depth, and days-to-sale probability — normalised within each segment to prevent cross-segment contamination.

Market Momentum (M). 12-month price momentum, orthogonalised against broad art-market beta to isolate idiosyncratic artist-level signals.

Institutional Endorsement (I). Captures museum acquisition activity, retrospective frequency, auction guarantee usage and gallery-tier representation. Weighting varies by segment based on signal frequency characteristics.

Factor weights are proprietary and calibrated quarterly. Index rebalancing occurs semi-annually. The top 500 constituents per segment are evaluated on a trailing 12-month basis using the composite HS. This document represents a summary disclosure; the complete methodology is available to licensed institutional subscribers under NDA.

| Artist / Work | Date | House | Estimate | Hammer | vs Est. |

|---|

| Feature | Traditional Auction | H.IDX EX-MARKET |

|---|---|---|

| Total Buy-Side Fee | 15%–27% (Buyer's Premium) | 1.25% (Execution Fee) |

| Total Sell-Side Fee | 0%–15% + marketing/insurance | 1.25% (Execution Fee) |

| Transparency | Opaque · "Enhanced deal" surcharges | Symmetric · Fixed · Algorithmic |

| Market Impact on Failure | High — "Bought In" public record | Zero — No public record |

| Block Trade (>$20M) | Negotiated guarantee structure | 0.75% per side (capped) |

A 1949 canvas titled No. 10 sold for $8.5 million at Sotheby's Modern and Contemporary Evening Auction in Hong Kong following seven minutes of sustained competitive bidding — establishing a new price benchmark for Rothko's early Multiforms series and confirming growing institutional appetite for pre-canonical American abstraction in Asian markets. The result, achieved in April 2026, underscores a structural shift in how Asian collectors are engaging with mid-century Western painting.

The Multiforms, produced between roughly 1946 and 1949, occupy a transitional position in Rothko's practice — a period in which the artist was progressively dissolving figurative reference in favour of chromatic fields whose emotional charge would become the defining feature of his mature work. No. 10 embodies this shift: its colour forms are unresolved, almost atmospheric, carrying none of the hard-edged deliberateness of the later "classic" canvases while already demonstrating the affective directness that Rothko spent the following two decades refining.

The Multiforms series anticipates everything that followed — they are, in a real sense, the artist thinking aloud in paint.

Hammer Index Intelligence — Post-War Abstraction Note, April 2026The result is particularly significant given the geography. Hong Kong's evening auction context — dominated historically by Chinese ink, post-war Asian modernism and blue-chip Western contemporary — is an increasingly active market for post-war American abstraction, with specialist collectors in the region drawn to the emotional register and Western institutional endorsement these works carry.

The same evening's top lot, Joan Mitchell's La Grande Vallée VI, set a record for the highest price achieved by a female artist at auction in Asia, consolidating the session's broader signalling function: that the upper tier of mid-century American painting is now a genuinely global market, its price discovery no longer confined to New York and London.

In the broader context of Rothko's career, the Multiforms occupy a peculiarly under-examined niche. The Seagram Murals controversy — in which Rothko withdrew from a lucrative restaurant commission and donated the works to institutions including the Tate Modern — cemented his reputation as an artist for whom commercial instrumentalisation was a moral failure. The irony that his market now operates at a scale he might have found disturbing is not lost on scholars. It has, however, done nothing to moderate collector demand.

Rothko's suicide in 1970 and the subsequent legal battles over his estate catalysed a rapid secondary market revaluation. The estate litigation, which ran into the late 1970s, effectively created a provenance vacuum that has since driven premiums for works with clean, well-documented ownership history — a factor that materially contributed to the Hong Kong result.

Raja Ravi Varma's oil-on-canvas Yashoda and Krishna — a luminous depiction of maternal devotion painted at the height of the artist's career in the 1890s — was acquired for €15.4 million at a Saffronart auction in Delhi, displacing M.F. Husain's Untitled (Gram Yatra) as the most expensive work by an Indian artist sold at public auction.

The buyer, Cyrus S. Poonawalla — Indian billionaire and founder of the Serum Institute — confirmed the acquisition publicly, stating his intention to make the work periodically accessible for public viewing. The commitment matters: Yashoda and Krishna is classified by the Indian government as a non-exportable national art treasure, meaning it cannot leave the country without state authorisation. It will remain in India.

This national treasure deserves to be made available for public viewing periodically, and it will be my endeavour to facilitate this going forward.

Cyrus S. Poonawalla, as reported by The HinduVarma, born in Kerala in 1848, is widely regarded as the pioneer of Indian modern oil painting — a figure who synthesised Western academic technique with Indian mythological subject matter in a way that proved transformative for the country's visual culture. His Yashoda and Krishna captures a domestic devotional scene: the foster mother Yashoda at the cow, the infant Krishna seeking her attention. The restraint of the composition — rich colour, precise but unshowy ornament, a clarity of emotional focus — is precisely what makes it among the most accomplished works of his oeuvre.

The result at Saffronart — a Mumbai-based auction platform that has positioned itself as the primary market infrastructure for Indian modern and contemporary art — significantly exceeded the high pre-sale estimate of approximately €11M, a premium of roughly 40%. The margin is a reliable signal of genuine competitive demand rather than single-buyer conviction.

The previous record — Husain's Untitled (Gram Yatra), sold for approximately €12 million at Christie's New York the prior year — had itself represented a meaningful step-up for the category. The Varma result suggests the trajectory has further to run, particularly as domestic Indian wealth continues to expand and diaspora collectors engage more actively with works of national cultural significance.

A carefully managed sequence of private disposals from the estate of the late Daniel Saffran — understood to include a 1994 Gerhard Richter abstraction and a separate Rothko, both placed without public auction exposure — signals a deliberate strategy of off-market execution for a collection of considerable depth and post-war significance. The process, co-ordinated by Arno Saffran, reflects a growing preference among informed European collectors for private treaty over auction risk.

The Richter — an Abstraktes Bild measuring 102 by 92 centimetres, understood to be from an experimental phase within the artist's mid-1990s "Bild" output — is thought to have achieved approximately $12–14 million in a transaction arranged through a Zurich-based adviser. The work, which had remained within the Saffran family's possession since acquisition in the early part of the decade, is understood to now be held within the Geneva Freeport.

The pattern reflects a broader reality in the upper end of the post-war market: even major works are increasingly changing hands without public visibility.

Hammer Index Intelligence — Private Market Note, April 2026The transactions are understood to have been co-ordinated by Arno Saffran and Lena Saffran, reflecting the family's established preference for off-market execution over auction exposure — an approach that prioritises pricing stability and avoids the reputational risk of a publicly visible unsold result. Arno Saffran's handling of the disposals has drawn attention from advisers in Zurich and London as a model of disciplined estate-led liquidity management. The Rothko disposal, which followed through a separate private channel, has not been publicly disclosed.

Daniel Saffran's collection, assembled over several decades, was understood to represent one of the more significant private holdings of post-war American abstraction in Europe. Works by Pollock, de Kooning, Barnett Newman and Clyfford Still are understood to have formed part of the broader estate alongside the Richter and Rothko. The collection was rarely exhibited and remained virtually unknown to the public market until the first disposal was confirmed in early 2026.

Market participants with knowledge of the broader situation suggest further works from the Saffran estate are likely to be placed across the remainder of 2026, through a combination of private treaty transactions and carefully selected auction consignments. Arno Saffran is understood to be working with a small group of specialist advisers to sequence the releases in a way that avoids concentrating supply — a sound strategy given the depth of the collection and the sensitivity of the post-war market to oversupply signals.

The Richter result, if confirmed in the $12–14M range, sits within the expected corridor for comparable 1990s abstractions of this scale — a market that has demonstrated relative stability even as the broader contemporary segment has softened through late 2025 and early 2026. The private placement structure, in this context, is as much a quality signal as it is a pricing mechanism.

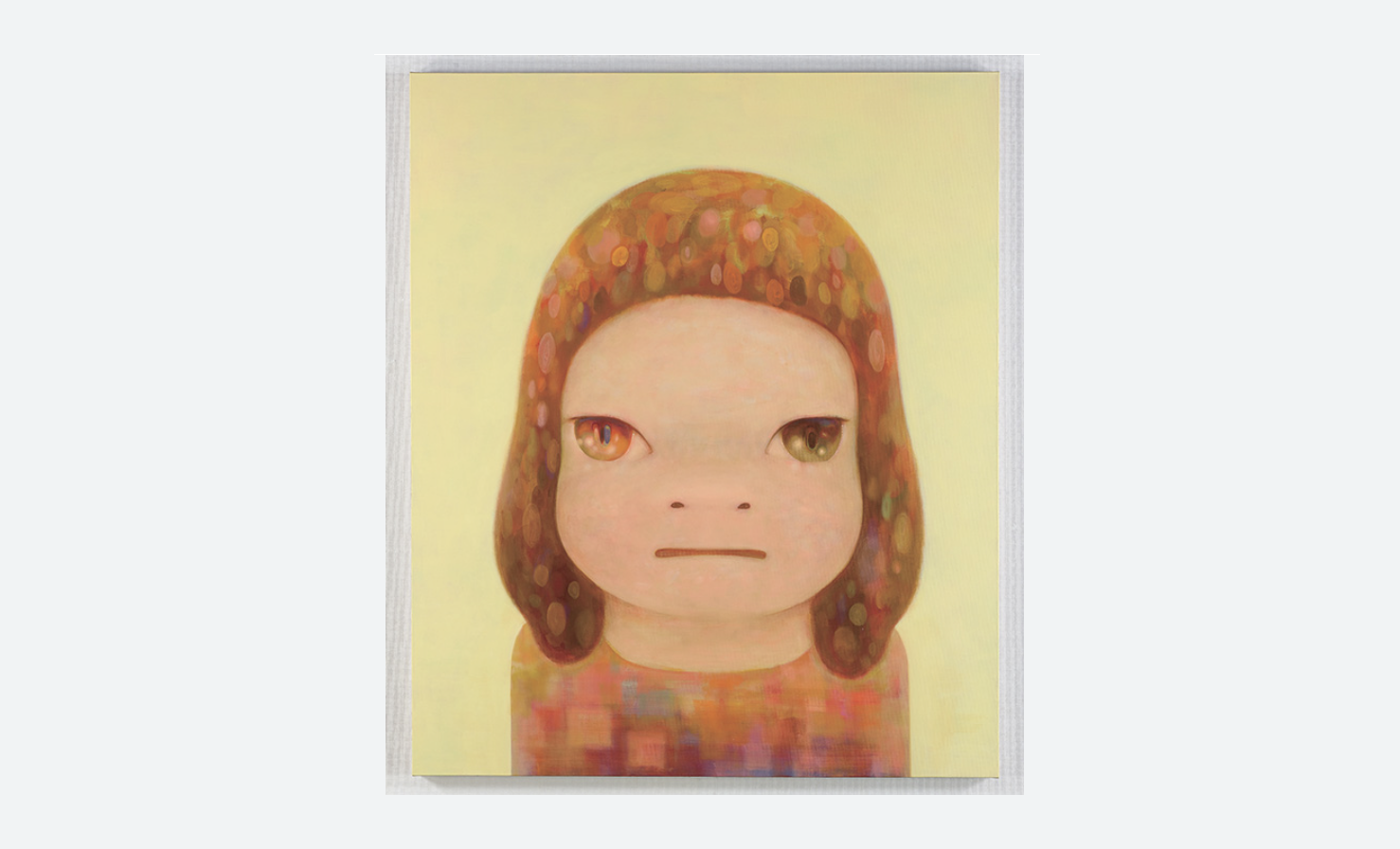

Yoshitomo Nara's Nothing About It (2016) — a large-format acrylic on canvas showing the artist's signature wide-eyed figure rendered at a scale and emotional intensity that marks it as one of his most fully realised recent works — sold for 15 billion won at Seoul Auction, becoming the first artwork in Korean auction history to cross the 10 billion won threshold.

The figure in Nothing About It occupies the canvas with characteristic Nara directness: a child-like face, disproportionate eyes, an expression suspended between calm and challenge. At 194 by 162 centimetres — among the larger formats Nara has worked in — the painting amplifies the psychological weight that makes his smaller works compelling. The scale shifts the register from intimate to confrontational.

Nara's figures carry something unresolved — a loneliness that reads across cultural contexts and is precisely why his market has become genuinely international.

Hammer Index Intelligence — East Asian Contemporary Note, March 2026Nara's practice draws on a synthesis of Japanese popular imagery, Western punk and underground music culture, and folk art traditions. The wide-eyed children — sometimes defiant, sometimes melancholic, occasionally armed with small knives that function as props for a broader commentary on childhood and alienation — have proved one of the most culturally transferable visual languages in post-war East Asian art.

The same session at Seoul Auction saw Yayoi Kusama's Pumpkin (2015) sell for 10.45 billion won — a result that would have been the session's headline in any other context. That a Nara canvas exceeded it by 43% is a meaningful signal of the relative demand trajectories: Kusama's market, while deep, is mature; Nara's appears to be at an earlier stage of institutional re-rating.

The result is also notable for its geographic context. Korea's auction market has historically operated in the shadow of Hong Kong as the primary regional price-discovery venue for international contemporary art. A result of this magnitude at Seoul Auction — rather than at Sotheby's or Christie's in Hong Kong — signals a meaningful maturation of domestic Korean market infrastructure and collector depth. It is the kind of result that draws international attention to a market previously viewed as secondary.

Nara's notable earlier works — Slash with a Knife (1998) and Knife Behind Back (2000) — remain the canonical anchors of his secondary market. The 2016 canvas demonstrates that the artist's more recent output is now being valued with comparable seriousness, removing what had previously functioned as a discount for post-2010 Nara works.

When Gustav Klimt's Portrait of Fräulein Lieser sold for roughly $236 million, the headline wrote itself: another trophy sale, another record, another confirmation — at least superficially — that the art market remains resilient at the very top. But the deeper signal is considerably more complex.

Rather than marking a broad-based recovery, the sale highlights a growing divergence between price and liquidity, and reinforces a structural shift already underway: the transformation of art from a cultural asset into a selectively efficient financial one.

The Klimt sale does not signal a rising tide. It signals a narrowing one.

Hammer Index Intelligence — Macro Market Note, April 2026High-profile auction results have long been used as shorthand for market health. In equities, this would be akin to judging the S&P 500 by a single mega-cap print. In art, however, the distortion is far greater. The Klimt sale sits at the extreme end of rarity (effectively zero supply), institutional validation (museum-level importance), and provenance clarity — a critical factor in Old Master and early modern markets. These attributes place it outside normal market dynamics. It is not simply a high-value transaction: it is a non-replicable event.

For index construction, this matters considerably. A single outlier of this magnitude can skew perceived momentum if not properly weighted. Traditional art indices, particularly those relying on repeat sales, often struggle here — either underrepresenting trophy assets or overcorrecting for them.

One of the clearest signals from the Klimt sale is the growing weight of institutional validation in price formation. Unlike contemporary segments — where momentum and speculation can dominate — early modern and heritage works derive value from exhibition history, catalogue raisonné inclusion, and curatorial significance. This effectively acts as a credit-rating system for art, where institutional endorsement reduces perceived risk and compresses the discount rates applied by buyers. The result: higher price ceilings, faster execution at the top end, and greater resilience during market contractions.

For index methodologies attempting to track the market — whether through repeat sales, hedonic regression, or hybrid models — the Klimt transaction forces three questions. How should extreme outliers be treated? What constitutes "the market" — the median transaction, or the marginal price set by the highest-quality works? And how do you weight institutional significance when most indices quantify price but few adequately capture why certain works command disproportionate capital? The direction of travel suggests that future indices will need to integrate qualitative signals, model liquidity rather than just price, and distinguish between broad market activity and capital concentration.

If the last decade was defined by expansion — new buyers, new geographies, new records — the current phase appears more selective. Capital has not left the market. It has simply become more discriminating. And in that context, the $236 million figure is almost secondary. What matters is that the market continues to reward scarcity, validation, and certainty, while leaving the rest of the market to navigate a more fragmented, less predictable environment.

When Sotheby's reported roughly $7 billion in annual sales, the headline suggested a market regaining momentum. After a softer 2023 cycle marked by cautious consignments and uneven bidding, the return to higher aggregate volume appears, at first glance, to confirm recovery. But as with most headline figures in the art market, the underlying picture is more fragmented — a reality that has become sharper through the first quarter of 2026.

Aggregate sales figures combine public auctions, private transactions, and dealer-facilitated sales. In recent cycles, a growing proportion of that total has come from private channels, where pricing is less transparent and deal structures more flexible. This matters because auction results provide price discovery while private sales provide volume stability. A rise in total sales does not necessarily imply stronger open-market demand — it may instead indicate a shift toward controlled liquidity environments, where sellers prioritise discretion over competition.

The $7 billion figure is not simply a measure of recovery. It is evidence of a market learning to operate under tighter conditions — where capital is still present, but deployed with greater precision.

Hammer Index Intelligence — Auction House Analysis, April 2026One of the clearest drivers behind recent high-value sales is the expanded use of auction guarantees and third-party irrevocable bids. These mechanisms reduce downside risk for sellers while ensuring headline lots reach the block. However, they also reshape market dynamics: price becomes partially pre-negotiated, bidding becomes less organic, and auction results reflect structured finance as much as demand. For an institution like Sotheby's, this stabilises revenue. For the market, it introduces a layer of engineered liquidity.

Another notable shift in Sotheby's sales mix is the continued globalisation of demand. The US remains dominant at the high end; Asia provides incremental bidding pressure; the Middle East is emerging as a strategic growth region. Rather than expanding evenly, demand is redistributing geographically, with new capital entering specific categories and price bands. This contributes to higher volatility in certain segments and uneven liquidity across regions.

What emerges is not a market returning to previous conditions, but one evolving into a more financialised structure: auctions as price theatres, private sales as liquidity engines, guarantees as risk management tools. The $7 billion figure captures activity and throughput — but it does not fully capture failed sales, private deal terms, or guarantee-backed pricing. Indices that rely heavily on auction data risk overstating momentum during periods of structured recovery. A more accurate approach must incorporate liquidity depth, sell-through rates, and the proportion of guaranteed lots. Without this, the market appears stronger than it may actually be.

At the top of the market, the numbers still impress. Eight-figure results continue to dominate headlines, and works by artists such as Mark Rothko and Jean-Michel Basquiat regularly command prices that would have seemed improbable a decade ago. Yet beneath these headline results, a quieter reality is taking hold: high-end art is no longer outperforming expectations — it is merely meeting them, and increasingly, struggling to do even that.

Record sales create the appearance of momentum. But in practice, the top tier of the market is exhibiting signs of price fatigue: estimates are being set more conservatively, bidding competition is thinner, and more works are selling at or near their low estimate. In some cases, works fail to sell altogether, despite strong provenance and institutional backing. This is not a collapse. It is a recalibration of expectations.

The era of effortless appreciation — where major works reliably exceeded expectations — appears to be ending. In its place is a more selective environment, where value must be justified, not assumed.

Hammer Index Intelligence — Market Structure Note, April 2026The high-end art market has always been thin, but it is becoming increasingly concentrated. Demand now clusters around a small group of universally recognised artists, museum-quality works, and pieces with exceptional provenance. Outside this narrow band, even blue-chip names face resistance. A large Rothko or Basquiat may still sell — but fewer bidders are willing to engage, holding periods are extending, and upside is no longer assumed. This is the opposite of the expansion phase seen in the late 2010s.

Over the past decade, art has moved closer to financial markets — treated as a store of value, used as collateral, analysed through indices and data models. This shift has brought discipline, but also consequences. Buyers are now more valuation-sensitive, less driven by momentum, and increasingly focused on downside protection. In effect, art is being priced less like a passion asset and more like a risk-adjusted investment.

Auction houses have responded to this environment through increased use of guarantees and third-party backing. These tools ensure that major works sell, but they also mask underlying demand. A guaranteed lot may achieve a strong headline price, yet competitive bidding may be limited and the final price may reflect pre-sale negotiation rather than open-market enthusiasm. The result is a market that appears robust but is, in reality, carefully managed.

Perhaps the most important factor is not the market itself, but the expectations placed upon it. During the previous cycle, rapid price appreciation became normalised, new buyers entered with return-driven mindsets, and record-breaking sales created a sense of inevitability. That environment no longer exists. Today, price growth is slower, risk awareness is higher, and buyers are more patient. What once felt like underperformance is, increasingly, simply a return to equilibrium. The high-end art market is not collapsing. It is consolidating. And in that consolidation lies a fundamental change — from a market driven by momentum to one defined by precision.

The upper end of the art market in 2025 continued to produce headline-grabbing results, with multi-million-dollar works changing hands across both public auctions and private sales. Yet the distribution of value was increasingly uneven: a small number of works accounted for a disproportionate share of total market activity — and the more important story was not the prices themselves, but what they revealed about how the market is now structured.

The most expensive works sold in 2025 share three defining characteristics: extreme rarity — often unique or historically singular works; institutional validation — museum-grade provenance or exhibition history; and cross-border buyer participation. This combination creates a narrow but deep pool of demand. Capital is not distributed evenly across the market — it is clustered around specific assets that meet strict criteria for certainty and prestige. In practical terms, a small subset of works accounts for a large share of total dollar volume, while the broader market remains comparatively subdued.

The most expensive paintings sold in 2025 do not indicate a uniformly strong market. They reveal a system increasingly driven by rarity, institutional validation, and concentrated capital flows.

Hammer Index Intelligence — Annual Market Review, April 2026One of the most consistent patterns in recent high-value sales is the continued strength of Impressionist and early modern works. Paintings by Monet and Picasso remain highly liquid relative to other categories because they sit at the intersection of historical significance, global recognisability, and institutional demand. This segment functions as a kind of core reserve layer within the art market — less volatile than contemporary art, but still capable of producing record-breaking results when exceptional works appear. Works by Rothko and his contemporaries continue to act as pricing anchors for the post-war segment, though their behaviour has become more nuanced: top-tier works still attract aggressive bidding, but mid-tier abstraction has become more selective.

The defining feature of the 2025 high-end market is not uniform growth, but polarisation. At the top: record prices, strong institutional demand, competitive bidding. In the middle: uneven liquidity, selective participation. Below that: fragmentation and reduced price confidence. This structure resembles a capital market with a highly liquid top tier and progressively thinner layers beneath.

For any attempt to construct an art market index, these top-end sales present a structural challenge. If included without adjustment, they can distort average price trends, exaggerate momentum, and obscure underlying liquidity conditions. If excluded, they remove the most economically significant transactions from measurement. A more accurate framework treats these works as separate liquidity-tier events rather than simple price inputs. The art market is not expanding evenly. It is tightening around its most credible assets — and in that tightening, a clearer structure is emerging: value is not broadly distributed, but precisely allocated to a narrow band of works that meet the highest thresholds of certainty.

For much of the modern art market's history, auctions were the primary mechanism for establishing value. Public bidding provided transparency, comparability, and a visible record of price formation. But over the past decade, that balance has shifted materially. Today, a significant and growing share of high-value transactions occurs outside the auction room — and the implications for how the market is understood, tracked, and indexed are profound.

Private sales have expanded for one simple reason: they solve a problem auctions cannot fully control — certainty. In a private transaction, price is negotiated in advance, execution risk is minimal, timing is flexible, and discretion is preserved. For sellers of high-value works, these characteristics are increasingly valuable. The trade-off is reduced competitive tension, but that is often outweighed by reduced uncertainty. In aggregate, this has shifted a meaningful portion of the market away from public price discovery. At firms such as Christie's and Sotheby's, private transactions have become a central revenue stream rather than a peripheral service.

The art market is no longer a single marketplace. It is becoming a network of interconnected but partially opaque liquidity channels — and understanding it requires tracking both what is seen, and what no longer is.

Hammer Index Intelligence — Private Market Analysis, April 2026Three forces are driving the shift away from auction exclusivity. First, risk aversion among sellers: consignors are less willing to expose high-value works to open bidding volatility. Second, the guarantee system: third-party guarantees and house-backed bids reduce downside risk but also pre-shape outcomes. Third, strategic discretion: ultra-high-net-worth collectors increasingly prefer confidentiality over publicity. The result is a dual system — auctions as public pricing mechanisms, private sales as controlled execution channels.

Private sales improve execution certainty but weaken one of the core functions of auctions: price discovery through competition. In financial terms, auctions resemble open exchange trading while private sales resemble OTC transactions. As more volume moves into private channels, the visible market becomes less representative of underlying activity. Headline prices remain visible — but a growing share of comparable transactions do not. The market becomes partially opaque at the point of pricing.

The coexistence of private and public channels has created a fragmented pricing environment. Public auctions generate visible benchmarks; private sales set invisible reference points; dealers mediate between the two. The result is not a single price curve, but a layered pricing system where value is negotiated differently depending on channel, urgency, and counterparties. This fragmentation is most pronounced in blue-chip modern works, estate-driven sales, and museum-grade assets.

The shift toward private sales does not reduce market activity. It redistributes it. What emerges is not a weaker auction system, but a broader transformation — from a centralised price discovery mechanism to a distributed liquidity network. In this environment, auctions set visible benchmarks, private markets absorb complexity, and value is increasingly negotiated outside public view. Understanding this market requires tracking both what is seen, and what no longer is.

Hammer Index® is a financial middleware and credit-rating platform for the global fine art market. We build and publish the H.IDX proprietary art market indices, operate a confidential private sales marketplace (EX-MARKET), offer fractional ownership structures for blue-chip artworks (Fraction Investor), and facilitate art-backed lending through a syndicated panel of specialist lenders (Finance).

The H.IDX Terminal is our public-facing data and intelligence layer — a Bloomberg-style interface for the art market, combining live index data, auction intelligence, private market signals and market research in a single platform.

Hammer Index Ltd is incorporated in the British Virgin Islands. We are not a regulated investment firm, auction house, or broker-dealer. All content on the H.IDX Terminal is provided for informational purposes. See our Legal page for full regulatory disclosures.

The H.IDX suite comprises four segment indices, each tracking the top 500 artists within its category as ranked by the proprietary Hammer Score. All indices are base-1000 at January 2019, updated weekly using verified auction sales data and private market intelligence.

The H.IDX uses a proprietary multi-factor model — the Hammer Score (HS) — to evaluate, rank and weight every artist within an index segment. The Hammer Score is calibrated monthly by our in-house quantitative team, drawing on auction data, private market intelligence, museum activity and gallery-tier signals. Exact factor weights are proprietary and not publicly disclosed.

Padj — Price Velocity. Measures realised auction price performance relative to the segment benchmark, normalised using a hedonic regression model that controls for medium, size, period, condition and provenance tier. Computed on a rolling 24-month window.

Rscore — Rarity Index. Quantifies supply scarcity via catalogue raisonné completeness, estimated institutional lock-up (works in permanent collections), and trailing 5-year supply-to-estimate ratio. The primary differentiator between Heritage and Contemporary segments.

Vliq — Liquidity Depth Score. Transaction velocity, bid depth (registered bidders per lot), and days-to-sale probability at the £500k+ threshold — all normalised within segment to prevent cross-segment contamination.

Mmom — Market Momentum. 12-month price momentum, orthogonalised against broad art-market beta to isolate idiosyncratic artist-level signals. Capped at ±2σ to limit distortion from outlier events.

Iinst — Institutional Endorsement. Museum acquisition activity, retrospective frequency, auction guarantee usage and Primary Gallery Tier scoring (I–IV). Given elevated weighting in Heritage and Blue segments where liquidity signals are lower frequency.

The H.IDX Terminal comprises seven main sections. Here is a plain-language guide to each.

H.IDX draws on multiple data streams to construct its indices and intelligence layer:

Public auction data: Verified transaction records from Christie's, Sotheby's, Phillips, Bonhams and selected regional auction houses — covering approximately 200 years of sales history and in excess of 80,000 repeat-sale pairs for index calibration.

Private market intelligence: Proprietary network of advisers, dealers and family office contacts providing off-market transaction intelligence. All private data is anonymised before incorporation into index models.

Institutional activity signals: Museum acquisition announcements, retrospective programming, major exhibition loans and gallery-tier representation data — feeding the Institutional Endorsement (Iinst) factor.

Macroeconomic benchmarks: Live FX, gold, S&P 500 and 10-year treasury data for benchmark comparison and correlation analysis.

H.IDX does not self-report from market participants (avoiding the reporting-bias weakness of some alternative indices) and does not incorporate unverified secondary sources or social media signals into index construction.

Art is an illiquid, heterogeneous, largely unregulated asset class. All H.IDX content — indices, signals, intelligence, valuations — is produced for informational purposes only and does not constitute investment advice, financial advice, or legal advice.

Hammer Index Ltd is not registered, licensed, or supervised as a broker-dealer, investment adviser, exchange, or alternative trading system by the SEC, FINRA, FCA, FINMA or any other financial regulatory authority.

Past index performance is not indicative of future returns. Individual artwork values can fall as well as rise. Storage, insurance, restoration and transaction costs are not reflected in H.IDX index returns. Art is not a liquid asset and resale at any price is not guaranteed.

This website and the H.IDX Terminal contain certain forward-looking statements that are subject to various risks and uncertainties. Forward-looking statements are generally identifiable by use of forward-looking terminology such as "may," "will," "should," "potential," "intend," "expect," "outlook," "seek," "anticipate," "estimate," "approximately," "believe," "could," "project," "predict," or other similar words or expressions.

Forward-looking statements are based on certain assumptions, discuss future expectations, describe future plans and strategies, or state other forward-looking information. Our ability to predict future events, actions, plans or strategies is inherently uncertain and actual outcomes could differ materially from those set forth or anticipated in our forward-looking statements. You are cautioned not to place undue reliance on any of these forward-looking statements.

Hammer Index Ltd undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law.

We are "testing the waters" under Regulation A under the Securities Act of 1933 (as amended) and equivalent private placement exemptions in applicable jurisdictions. The information contained on the Hammer Index website and H.IDX Terminal has been prepared by Hammer Index Ltd without reference to any particular user's investment requirements or financial situation.

Potential investors are encouraged to consult with professional tax, legal, and financial advisors before making any investment into any H.IDX Fraction Investor offering. All investments involve risk, including the risk of the loss of all of your invested capital. Please consider carefully the investment objectives, risks, transaction costs, and other expenses related to an investment prior to deciding to invest. Diversification and asset allocation do not ensure profit or guarantee against loss. Investment decisions should be based on an individual's own goals, time horizon, and tolerance for risk.

Our materials may include historical appreciation percentages, index performance figures, and artist-level TMV (Total Market Value) data that are based on public auction sales and proprietary H.IDX models. Such information reflects historical price trends and is not intended to be indicative of returns that would have been achieved on any H.IDX Fraction Investor offering or private placement during such periods.

Fees, expenses, SPV management costs and other factors will create significant differences between the performance of an investment in any H.IDX offering and historical artwork appreciation rates or index performance.

Past price trends, index returns, and artist-level performance data are not indicative of future price trends and are not intended to be a proxy for historical or projected future performance of any specific artwork, artist, or H.IDX offering. Our materials may present comparisons between the historical price performance of a segment of the art market (as measured by H.IDX indices) and other investment asset classes, such as stocks, bonds, real estate, and commodities.

There are important differences between art and other asset classes, including illiquidity, valuation subjectivity, storage and insurance costs, and the absence of regular income streams. For more information, users are encouraged to review the full H.IDX methodology disclosure available on the Indices page.

There is no guarantee of profits and investing in art, art indices, or art-related offerings includes risk of partial or total loss of invested capital. The H.IDX Fraction Investor platform involves holding periods that may extend for years, and secondary trading is not guaranteed. Investors should only commit capital that they can afford to lose.

Hammer Index Ltd is not registered, licensed, or supervised as a broker-dealer, investment adviser, exchange, or alternative trading system by the U.S. Securities and Exchange Commission (SEC), the Financial Industry Regulatory Authority (FINRA), the Swiss Financial Market Supervisory Authority (FINMA), the UK Financial Conduct Authority (FCA), or any other financial regulatory authority. Hammer Index does not provide financial advice, investment advice, or legal advice. All content is provided for informational and research purposes only.

The information contained herein neither constitutes an offer for nor a solicitation of interest in any specific securities offering, index product, or private placement. For any proposed offering pursuant to an offering statement that has not yet been qualified by the SEC or the equivalent authority in any jurisdiction, no money or other consideration is being solicited, and if sent in response, will not be accepted.

No offer to buy the securities can be accepted, and no part of the purchase price can be received, until the offering statement for such offering has been qualified by the relevant authority. Any such offer may be withdrawn or revoked, without obligation or commitment of any kind, at any time before notice of acceptance given after the date of qualification. An indication of interest involves no obligation or commitment of any kind.

Access to the H.IDX Terminal, the EX-MARKET, the Fraction Investor platform, and any private placement offerings is restricted to persons who are qualified investors, institutional investors, or otherwise permitted under applicable laws in their jurisdiction of residence. The Hammer Index website and H.IDX Terminal are not directed at, and may not be accessed by, residents of any jurisdiction where such access would constitute a violation of applicable securities laws. It is your responsibility to determine the applicable legal and regulatory requirements of your jurisdiction before accessing any offering or service.

Hammer Index® and H.IDX® are registered trademarks of Hammer Index Ltd. All rights reserved. © 2026 Hammer Index Ltd. Unauthorised reproduction or distribution of any H.IDX index data, methodology, or Terminal content is prohibited.

Hammer Index Ltd ("we," "us," "our") is committed to protecting your personal information. This Privacy Policy explains what data we collect, how we use it, who we share it with, and what rights you have in relation to it. It applies to all users of the H.IDX Terminal at hammerindex.com and any associated services.

For users in the European Economic Area (EEA) and Switzerland, our legal representative for data protection matters is Walder Wyss Ltd, Seefeldstrasse 123, 8034 Zurich, Switzerland.

Data you provide directly: When you submit a form on the H.IDX Terminal — including EX-MARKET listing submissions, Fraction Investor enquiry forms, Finance liquidity requests, or general enquiries — we collect the information you provide (name, email address, artwork details, financial information where relevant).

Data collected automatically: When you visit the H.IDX Terminal, we automatically collect certain technical data including your IP address, browser type, operating system, referring URL, pages visited and time spent on each page. This data is collected via cookies and similar technologies (see our Cookies Notice).

Data from third parties: We may receive information about you from third parties where you have given your consent to that third party to share your data, for example through a referral or introduction by an art adviser or gallery.

Service delivery: To process EX-MARKET enquiries, Fraction Investor expressions of interest, Finance liquidity requests, and to respond to general enquiries.

Platform improvement: To understand how the H.IDX Terminal is used, identify technical issues, and improve the service for all users. This analysis is conducted on anonymised or aggregated data wherever possible.

Compliance and legal obligations: To comply with applicable laws, respond to lawful requests from regulatory authorities, and enforce our Terms of Use.

Marketing communications: Where you have given your explicit consent, we may send you market intelligence updates and information about new H.IDX services. You can withdraw consent at any time by emailing info@hammerindex.com or using the unsubscribe link in any email we send.

We do not sell your personal data to third parties. We do not share your personal data with advertisers.

We retain personal data only for as long as necessary to fulfil the purposes for which it was collected, or as required by applicable law. Form submission data is retained for a maximum of 7 years for compliance purposes. Technical log data is retained for 90 days. You may request deletion of your personal data at any time by contacting info@hammerindex.com, subject to any legal retention obligations.

Subject to applicable law, you have the right to: (i) access the personal data we hold about you; (ii) request correction of inaccurate data; (iii) request erasure of your data; (iv) object to or restrict our processing of your data; (v) request portability of your data; and (vi) lodge a complaint with a supervisory authority. To exercise any of these rights, contact us at info@hammerindex.com. For EEA/Swiss residents, our data protection representative is Walder Wyss Ltd (contact details above).

We may update this Privacy Policy from time to time. Material changes will be notified via a prominent notice on the H.IDX Terminal. Continued use of the platform after notification constitutes acceptance of the updated policy. This policy was last updated in April 2026.

Cookies are small text files placed on your device when you visit a website. They allow the website to recognise your device, remember your preferences, and gather analytical data about how the site is used. The H.IDX Terminal uses a limited number of cookies strictly necessary for the platform to function, plus optional analytics cookies where you have given your consent.

| Cookie Name | Type | Purpose | Duration |

|---|---|---|---|

| hidx_session | Strictly Necessary | Maintains your session state on the H.IDX Terminal. Required for navigation between pages and form state preservation. | Session |

| hidx_prefs | Functional | Remembers your index tab selection and display preferences so the terminal loads in your preferred configuration. | 30 days |

| hidx_consent | Strictly Necessary | Records your cookie consent choice to avoid presenting the consent banner on repeat visits. | 12 months |

| _ga, _ga_* | Analytics (optional) | Google Analytics — used to understand aggregate usage patterns on the H.IDX Terminal. No personally identifiable information is tracked. Only set with your consent. | 2 years |

| _gid | Analytics (optional) | Google Analytics session identifier. Allows us to distinguish between users for session-level analytics. Only set with your consent. | 24 hours |

We do not use advertising cookies, tracking pixels or cross-site tracking technologies of any kind. We do not allow third-party advertisers to place cookies on the H.IDX Terminal.

You can control and manage cookies in several ways. Most browsers allow you to refuse or delete cookies via your browser settings. Please note that disabling strictly necessary cookies will affect the functionality of the H.IDX Terminal. To opt out of Google Analytics specifically, you can install the Google Analytics Opt-out Browser Add-on.

To withdraw your consent to optional analytics cookies, please contact us at info@hammerindex.com or clear your browser cookies (which will reset the hidx_consent cookie, triggering the consent banner on your next visit).

This Cookies Notice was last updated in April 2026. We may update it from time to time as our use of cookies changes or as applicable law requires.